After 60 years of running Berkshire Hathaway (BRK.A 0.18%) (BRK.B 0.09%), Warren Buffett will be riding off into the sunset.

The 94-year-old, widely regarded as the greatest investor of all time, announced at Berkshire’s annual shareholder meeting over the weekend that Greg Abel would take over as CEO by the end of the year.

Buffett is regarded as an investing and business legend for a number of reasons, and Berkshire’s track record speaks for itself. He essentially doubled the annual return of the S&P 500 (SNPINDEX: ^GSPC) over his career, delivering phenomenal returns for his investors along the way.

Image source: The Motley Fool.

Arguably, Buffett was at his best during bear markets, and Berkshire’s greatest periods of outperformance often came during sell-offs. He built his conglomerate for longevity with durable, all-weather businesses like insurance companies, and the famed value investor was able to capitalize on stock market sell-offs and take advantage of deals in the private market as he often kept a large war chest of cash on hand to be ready when a good value presented itself.

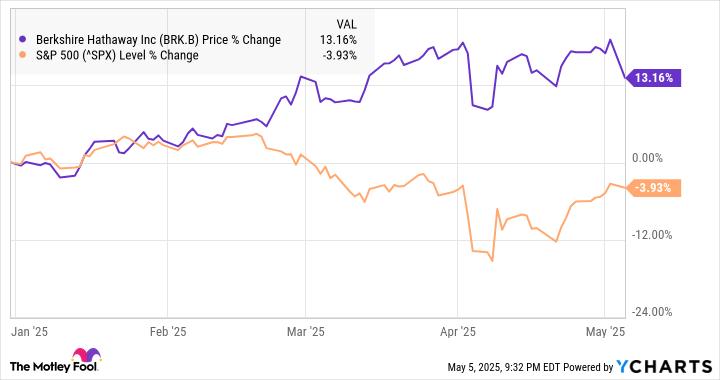

While we’re not in a bear market, the S&P 500 was on the verge of one not long ago, and 2025 has already given investors plenty of volatility. In this environment, Berkshire’s reputation for stability has served it well as it’s outperforming the S&P 500 by a wide margin, and the chart below includes the 5% decline after Buffett announced his retirement.

As good as Berkshire has been in bear markets under Buffett, there are a few other stocks that have been even better, outperforming Berkshire not just this year, but in prior years. Let’s take a look at two of them.

1. Altria

Altria (MO -1.61%) hasn’t been a top stock over the last decade, but its performance over its history has been dominant, especially when factoring in dividends reinvested.

Altria is currently the domestic seller of its Marlboro and other cigarette brands, as well as smoke-free products like on! oral nicotine pouches and NJOY vapes. Earlier in its history, it was a global company combined with Philip Morris International.

As a tobacco company, Altria has the advantage of selling a recession-resistant product, as smokers and other consumers of its products tend to buy them regardless of the state of the economy. Altria’s high-yield dividend and status as a Dividend King, having raised its dividend 59 times in the last 55 years, also makes it an attractive stock in a down market as it has reliably paid increasing dividends for nearly as long as Buffett’s been CEO.

On a total return basis, Altria stock is up 16.6% this year, outperforming both Berkshire and the S&P 500.

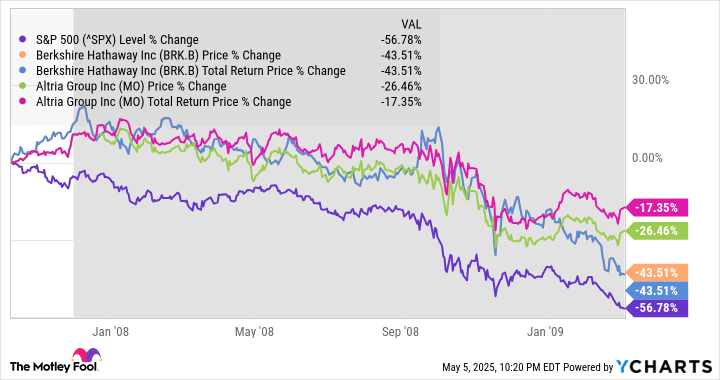

During the bear market of 2007-2009, during the financial crisis, Altria stock fell, but it still beat both Berkshire Hathaway and the S&P 500, as the chart below shows.

Though Berkshire stock held up well through the early stages of the bear market, it fell sharply in the fourth quarter of 2008 following the collapse of Lehman Brothers and as it reported large paper losses in its stock portfolio.

A business like Altria’s, on the other hand, doesn’t have to worry about that kind of volatility.

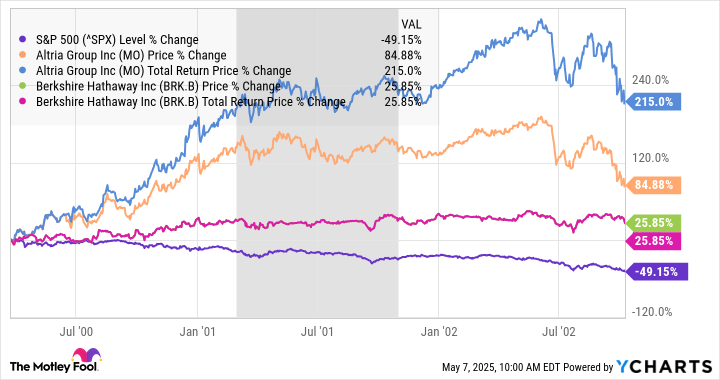

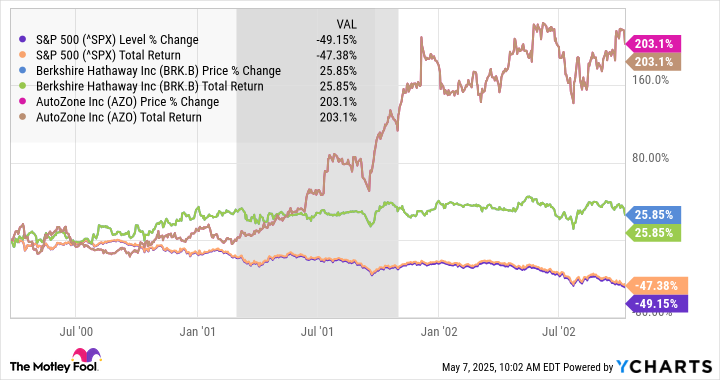

Similarly, during the bear market of 2000-2002, both Altria and Berkshire Hathaway delivered a positive return as they were relatively unaffected by the dot-com bust, even as the S&P 500 lost 49%. However, as the chart below shows again, Altria was the clear winner, tripling during that period when including dividends reinvested.

With its dividend yield of 6.8% today and its recession-proof business model, Altria looks like a good bet to outperform in a bear market if it happens again.

2. AutoZone

Another sector that has a clear track record of outperforming in bear markets is aftermarket auto parts.

After all, consumers generally buy these products because they need them for repairs, and in recessionary environments, they tend to delay replacing their vehicles and instead spend on repairs, meaning replacement parts. In other words, auto parts is a countercyclical industry, meaning consumers spend more on them in bad times than in good.

One of the best-performing stocks in that sector has been AutoZone (AZO -0.44%), which has steadily expanded its store base and excelled at managing inventory through its hub and spoke, where centrally located hub stores ensure that spoke stores remain well-stocked. That also helps it serve commercial customers like repair shops that need parts in a timely manner.

AutoZone has a history of capitalizing on recessions, and year to date, the stock is up 17.8%.

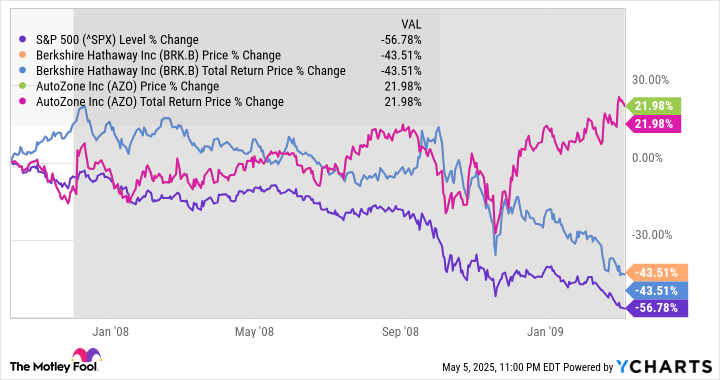

In previous bear markets, AutoZone has also thrived. In the 17-month bear market during the financial crisis, the stock gained 22%, as you can see from the chart below.

Historically, the business has accelerated toward the end of recessions, presumably because consumer savings have been depleted at that point. In fiscal 2009, which ended in Aug. 2009, domestic same-store sales rose 4.4%, its best performance in the previous five years.

AutoZone is not a dividend payer, but the company has aggressively repurchased its stock over its history, accelerating its earnings-per-share growth and boosting the stock price by taking advantage of discounts as they come.

In the 2000-2002 bear market, AutoZone stock also soared, tripling during that period like Altria. Again, its gains were weighted to the second half of the downturn.

Similarly, AutoZone’s comparable sales surged 9% in fiscal 2002, coming out of the recession of that era.

That pattern of outperformance is likely to hold up again if the economy slips into a recession, which explains why AutoZone is up nearly 20% this year on little news.

Is Berkshire still a buy?

Investors may be disappointed that Buffett is stepping down as the rare 5% slide in Berkshire stock indicates, but the Oracle of Omaha has built the company for the long term.

Additionally, Berkshire also benefits from a cash hoard that has swelled to nearly $350 billion, giving the company plenty of firepower to make a deal if it finds an attractive one.

Berkshire is certainly not a bad stock to own in such an environment and its unique position makes it a buy. However, investors looking to a capitalize on a potential bear market would do well to buy shares of Altria or AutoZone.

Both have history behind them, and their business models make them highly likely to beat the market again should it tip into a recession.

{kind=link}