The broader stock market continues to roar higher. But 11 of the 30 components of the Dow Jones Industrial Average are down this year.

The worst performers, in order, are Boeing (BA 0.61%), Intel (INTC 0.35%), Nike (NKE -6.90%), and Apple (AAPL 0.53%) — which may come as a surprise, since the broader semiconductor industry and many big tech growth stocks are flying high.

Here’s what’s dragging down each blue-chip stock, and why it could get worse before it gets better.

Image source: Getty Images.

Boeing must fix its major issues even at the expense of its near-term performance

Boeing has not had a good 2024. On Jan. 5, a Boeing 737-9 MAX door plug came off mid-flight. Since then, Boeing has been scrambling to restore confidence and ensure safety.

On Jan. 24, the Federal Aviation Administration (FAA) stated that it would halt Boeing MAX’s production expansion and investigate Boeing’s maintenance and quality control.

On March 4, the FAA “…found multiple instances where the companies allegedly failed to comply with manufacturing quality control requirements. The FAA identified non-compliance issues in Boeing’s manufacturing process control, parts handling and storage, and product control.”

On March 20, Boeing said that it would slow production and burn more cash in an effort to improve quality.

Cases like this are never good, especially when they have to do with safety. As for the company, Boeing’s 2025/2026 medium-term targets are in jeopardy. Boeing was guiding for $10 billion in annual free cash flow during that time frame, but it will probably miss that goal now.

Boeing continues to hit speed bumps along an increasingly uncertain runway. The stock got crushed during the COVID-19 pandemic as travel ground to a halt. It largely missed out on the broader market rally, and remains down over 57% from its all-time high.

Boeing used to be the most heavily weighted stock in the Dow. But now it is closer to the median. Investor patience is running out, and the stock could struggle before staging a turnaround.

Intel is moving in the right direction

Intel had a fantastic year in 2023, surging 90%. The recovery was mainly due to investor optimism that Intel is finally on track. But that doesn’t mean its precious wasted opportunities are completely forgotten.

Intel is an excellent example of why the top dog in a dynamic industry can lose its throne in a relatively short period of time. Intel lost market share in the CPU market and missed out on the AI-driven GPU boom. Intel believes it can unlock growth in the foundry business and become the second-largest foundry by 2030.

Size isn’t the only differencing factor. Supported by government funding, Intel is building foundries across the United States to onshore semiconductor production. This presents an opportunity for American chip makers to reduce the geopolitical risks of relying too much on Taiwan. Granted, Taiwan Semiconductor Manufacturing is also investing in U.S. fabs.

Intel stock was left for dead but now has hope. After last year’s run-up, it’s understandable why the stock would pull back given that much of its potential growth is years away.

Major challenges for Nike

Nike is facing two key threats. The first is slowing growth out of China. On its Q2 fiscal 2024 earnings call, Nike revised its full-year revenue guidance to just 1% growth compared to fiscal 2023. Softness out of China, Europe, the Middle East, and Africa was largely responsible for the revision.

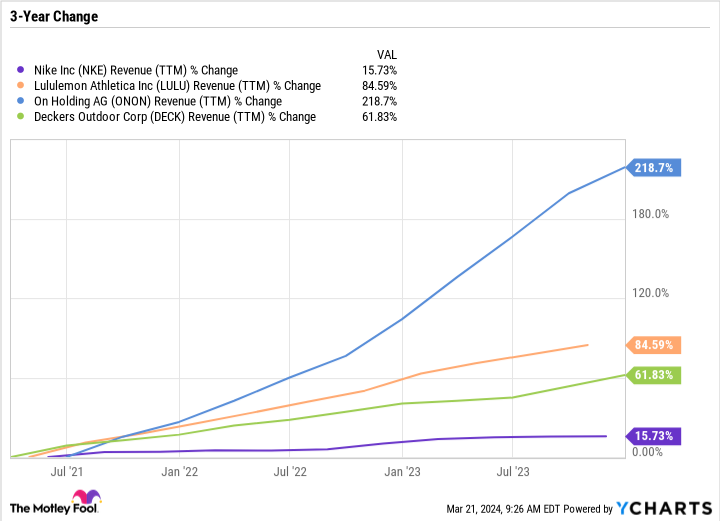

Nike has always dealt with competition, but it seems to be ramping up in recent years. Lululemon sustained breakneck growth and is now worth nearly 40% as much as Nike. Smaller footwear and apparel brands like On Holding and Hoka have taken the market by storm. Hoka is owned by Deckers Outdoor, which also owns UGG and Teva.

Nike is a bigger company, so moving the needle is harder. But still, trailing 12-month revenue is up just 15.8% over the last three years, which is a bad look compared to Lululemon, On, and Deckers.

NKE Revenue (TTM) data by YCharts

Nike relies heavily on massive marketing expenses and its brand. Perception is everything when it comes to charging a premium price for what is ultimately just a commodity.

The good news is that the valuation has come down. Nike’s price-to-earnings (P/E) ratio is now just 29.3, which is far lower than the five-year median of 34.6.

Nike is too good of a company to trade at a discount to the market. Value investors will eventually step in and swoop up shares, but the bulk of Nike’s sell-off thus far is justified.

Apple is pulling out the stops to offset slow growth

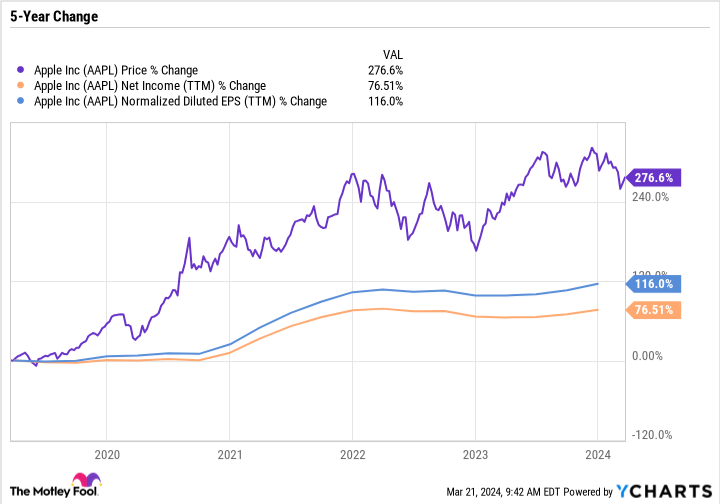

Apple’s sell-off also makes sense. The growth rate of the stock price has far exceeded profit growth, which has made the stock more expensive.

Apple is dealing with slowing growth out of China and decent growth elsewhere. However, optimistic investors hope that Apple has a hidden backlog in the form of customers who have older iPhone models and are overdue for an upgrade. This pent-up demand could help Apple get back on track. But the fact remains that iPhone sales growth slowed dramatically, and Apple’s business model still greatly depends on the iPhone. And a recent development demands attention — the Justice Department filed a lawsuit against Apple accusing it of illegally stifling competition and violating antitrust laws to keep customers reliant on their iPhones and less likely to switch to another device.

To its credit, Apple’s high-margin services segment is thriving and continues to put up record results. Apple also bought back a considerable amount of stock, which has helped its earnings per share (EPS) growth outpace net income growth. The impact of stock buybacks doesn’t always appear in the short term. But given the pace at which Apple repurchases shares, you can begin to see the divergence over the medium term.

Referring back to the chart, consider that Apple’s net income is up 76.5% over the last five years but EPS is up 116% thanks to buybacks. Apple’s steadfast buybacks make the stock a better value even when growth is slow.

Out of all the companies on this list, Apple stands out as the best long-term investment because parts of the business are doing well, it has a rock-solid balance sheet and plenty of cash to make an acquisition to fuel growth if needed, and it remains a market leader. In the meantime, Apple could continue underperforming the broader market until its fundamentals improve.

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Lululemon Athletica, Nike, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and On Holding and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, long January 2025 $47.50 calls on Nike, and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

{kind=link}