Well, folks – it’s here. Markets have been pricing in tariff concerns for weeks, and this afternoon we should be learning what the proposals are likely to entail. Each session this week has seen stocks bounce off their lows created by early selling. That activity implied that traders might be pricing in today’s announcement as a “sell the rumor, buy the news” event. It appears that view is widely held by options traders.

We have all heard the adage, “buy the rumor, sell the news.” In an IBKR podcast, I explained it this way:

…the efficient market hypothesis says that markets contain all the information that’s available to them and use that information to price whatever financial asset efficiently. In reality, that kind of works in the long term. It doesn’t necessarily work in the short term. So, what happens a lot of times is you hear that some company is going to be announcing some new product, let’s say the new iPhone for example, and everybody knows the new iPhone is going to be great and you hear all the rumors about the new features and what it’s going to encompass and everything else.

[When] it’s actually released … and the demand for it is what everybody expected, well, where’s your catalyst? The stock has presumably been going up because everybody’s been buying based on all this other stuff. Well, now it’s here. Who’s the next buyer?

That concept can work in reverse as well. If everyone widely expects a piece of news to be negative and investors price that in, the news needs to be even worse than expected for it to push prices lower. Otherwise, the reaction results in higher prices.

The key problem with today’s announcement is that no one has been quite sure exactly what to price in. When we have “known unknowns” there is typically a range of definable outcomes. Ahead of the last election there was uncertainty about the eventual winner, but investors could certainly create a playbook for a victory by either candidate. Ahead of a Fed meeting there are well-defined probabilities for the likelihood of a rate cut. Ahead of an earnings or economic report, such as Friday’s jobs numbers, there are well-disclosed consensus estimates. As I said to a reporter yesterday:

I can’t recall a situation where the stakes were this high and yet the outcome was so unpredictable. The devil is going to be in the details and nobody knows the details.

Regardless of that lack of clarity, traders of S&P 500 Index (SPX) options seem to be more concerned with missing a bounce than hedging a further decline. We see this in the IBKR Probability Lab data for SPX options expiring tomorrow and Friday:

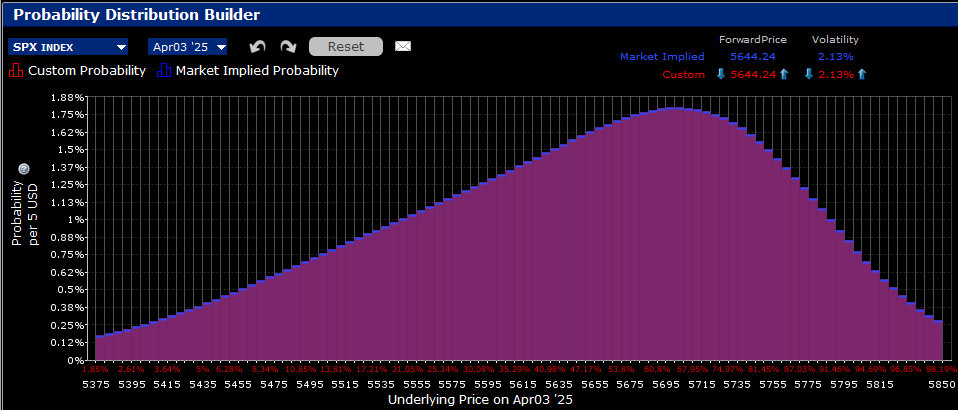

IBKR Probability Lab for SPX Options Expiring April 3rd, 2025

Source: Interactive Brokers

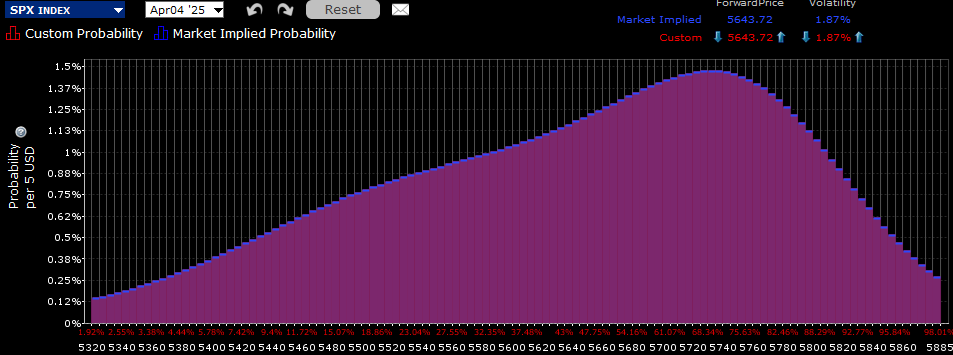

IBKR Probability Lab for SPX Options Expiring April 4th, 2025

Source: Interactive Brokers

It is quite clear that there is an upward bias to the curve, which tends to have something resembling a normal distribution. In both cases – the first is a relatively “pure” read on this afternoon’s tariff news, the second includes Friday’s employment report – we see that the peak probability is above current levels. The peak for tomorrow’s options is around 5715, about 1.2% above the current SPX level, and for Friday it is around 5745, or 1.8% higher.

That said, it is not as though SPX options traders are truly sanguine. We see at-money implied volatilities pricing in roughly 2.4% and 2.1% daily moves for tomorrow and Friday, respectively. Considering the potential magnitude of the tariff announcements, that shows respect for the likelihood of a substantial move. We also see curvy downside skews, but with some relative steepening. That implies at least a healthy respect for a potentially negative outcome.

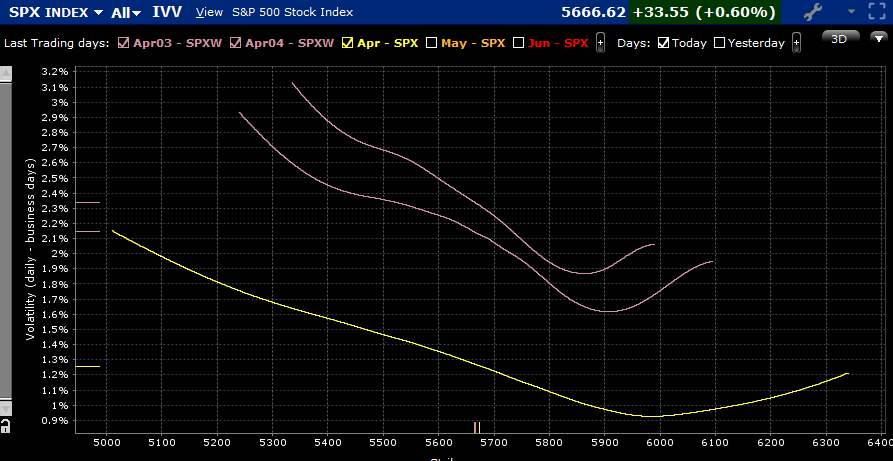

SPX Skews for Options Expiring April 3rd (top), April 4th (middle), April 18th (bottom)

Source: Interactive Brokers

And just in case you need a further reference for how skittish and illiquid the current market conditions might be, note that I took the Probability Lab and skew snapshots about 5 minutes apart. In that brief time, we saw SPX rally by about 20 points.

Buckle up. The first act of liberation could be a bumpy ride.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options (with multiple legs)

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by clicking the link below. Multiple leg strategies, including spreads, will incur multiple transaction costs. “Characteristics and Risks of Standardized Options”

{kind=link}